Retirement Transition: The Key Decisions You’ll Make

Getting married. Buying your first home. Having a baby. Few would debate the significance of these life events. But what about “retirement transition”?

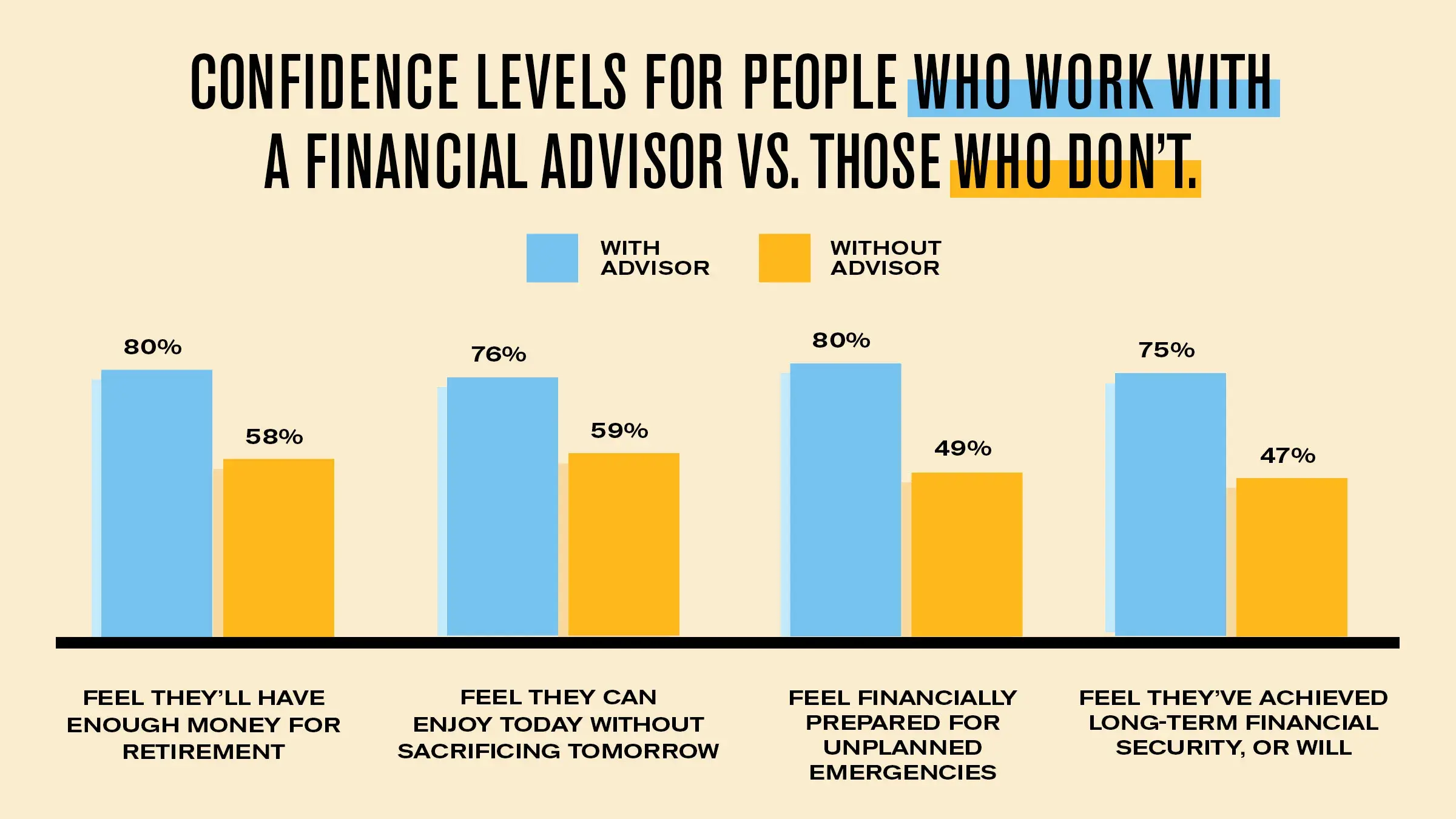

Participants in a 2023 Northwestern Mutual study1 of affluent pre-retirees and retirees indicated that the retirement transition might just have a place in this list. From contending with psychological challenges like parting with your professional identity to practical ones like deciding which medical plan best meets your needs or whom you’re going to spend your time with, you don’t want to underestimate the magnitude of this life change.

Indeed, during the retirement transition you’ll face numerous major life decisions in a short amount of time. What’s more, many of the choices you make during this time will have an outsized impact on the rest of your life. And according to renowned retirement and longevity expert Steve Vernon, the “rest of your life” after entering retirement could be as many as 20 to 30 years.

In the following discussion with Steve, he shares his knowledge on the significance of the retirement transition as well as the key decisions you’ll face during this major life change. Here’s our conversation.

Steve, you’ve written and spoken extensively on the idea that there are critical decisions that must be made as a person transitions into retirement. There is even something you call the “critical retirement decision zone.” What is that, and why is it important?

I believe the critical retirement decision zone for most people is between ages 60 and 70. During this time, they will make decisions that impact their quality of life for the rest of their lives. These decisions include when to retire, whether to work part time for a while, how to generate retirement income, whether to volunteer, where to live, how to improve their health, and whom they want to spend time with.

When you think about it, the period between ages 20 and 30 was a similar critical decision zone for most people. Fortunately, most pre-retirees and retirees now have much more life experience, and hopefully they can make more informed decisions.

At a high level, what do you believe are the key areas that must be considered during the retirement transition to help foster a long, healthy and financially secure retirement?

The foundations of a good retirement are financial security, good health, a robust network of supportive family and friends, and living a life of meaning and purpose. You’ll want to develop compelling reasons to get up in the morning, even into your 90s and beyond.

There are two important aspects of financial security:

-

Develop a portfolio of retirement income that lasts the rest of your life, no matter how long you live, and covers your living expenses in retirement.

-

Develop strategies to protect against common risks in retirement, which include health care and protection against frailty in your later years.

Finally, you’ll want to develop a strategy to protect yourself and your family if you become very frail in your later years. You might have increased costs for daily care, and you may be vulnerable to making financial mistakes due to diminished decision-making capacity. You’ll want to work with your financial advisor to develop strategies to address these risks.

One of the decisions many will make entering retirement is whether to continue working in retirement. But working in retirement seems like a big shift from prior generations, when retirement was essentially defined by the absence of work. Should folks plan to work in retirement? If so, why?

There can be several good reasons to continue working in your retirement years. First and foremost, many people might need or even just want the money. Income from working can help you delay starting Social Security and delay tapping into your retirement savings, both of which can be very desirable strategies.

However, there can be other good reasons to continue working. You might be eligible for health insurance, which can be very expensive if you buy it on your own before you’re eligible for Medicare at age 65. In fact, many retirees delay retiring until they are eligible for Medicare because they can’t afford or don’t want to pay for medical insurance on their own before then.

Working also can keep you active, keep your mind sharp and provide a social network.

The key to working in your retirement years is to find work that you like (or at least can tolerate) and avoid work that you don’t like. If you’re not yet retired, as a starting point, make a list of all the aspects of your current work that you like. See if you can find these aspects with potential retirement work. Make another list of all the aspects of your current work that you don’t like. Try to avoid retirement work that has these aspects, if possible.

You mentioned the importance of health and health care. And, according to our survey, both good health and health care affordability are weighing heavily on retirees’ minds, too. What key decisions should folks be considering regarding their own health and well-being? What about access to health insurance as they transition into retirement?

“Good health” is often near the top of the list of surveys that ask retirees about what makes them happy in retirement. While there are entire books written on this topic, it often boils down to these eight steps:

- Eating right for your body and health conditions

- Getting frequent and varied types of exercise

- Getting sufficient sleep

- Maintaining a healthy weight

- Minimizing stress

- Avoiding smoking or abusing alcohol or drugs

- Assembling a supportive team of health care professionals and developing, with your doctor, an early warning system of diagnostics and tests, along with recommended remedies for potential health issues

- Developing and maintaining a robust and supportive network of family and friends

Additionally, you’ll want to carefully choose your health insurance, both before and after eligibility for Medicare. You’ll want to learn about the differences between Medicare and the health insurance you enjoyed while working. Most people assume because Medicare is called “health insurance” that it’s the same as when they were working. Big mistake!

Medicare has larger deductibles and co-payments compared to most employer-sponsored health insurance. Also, Medicare doesn’t cover dental, hearing, long-term care and most vision expenses.

In your book Retirement Game Changers, you have a whole chapter on choosing the best place to live. Why is this such a significant decision to make as you enter retirement? What are the key considerations folks should be making?

A large home in the suburbs might have been a good place to raise a family and commute to work from. However, it may not be the best place for you once the kids are off the “payroll” and you’re no longer working.

Too many people stay in a house that they can no longer afford, is a burden to maintain or doesn’t fit their needs anymore. A typical example is a house with stairs that older people can no longer navigate. Often, I see older retirees suffer a health or financial shock, and suddenly they need to move. At that time, they may be too frail to make the move on their own, and they need to rely on family and friends. Instead, I recommend that retirees anticipate if this or other situations could happen to them and then make a move while they still have the capability and means to do so.

I also suggest that retirees consider both the community and house that might better fit their needs. Look for situations where you can get your daily exercise by walking out the door or riding your bike. Make it easy to meet friends or run errands. Make sure your health care providers aren’t too far away.

You can find lists of factors to consider when choosing where to live in the chapter of my book, Retirement Game Changers, that you mentioned.

When thinking about retirement, many of us imagine what we can be doing with our newfound freedom. But the reality is, as we age, there will likely come a time nearer the end of our lives when we grow frail. You recommend that decisions about that time also be made when entering retirement. What are the critical decisions folks need to be thinking about as they relate to this period?

You’ll want to consider the time in your life when you might be frail and will need help with basic activities of daily living, such as preparing meals, cleaning your house, showering, using the bathroom, taking medications and simply moving around. It can be very expensive if you need to pay someone to help you or if you need to move to an assisted living facility. You’ll want to make sure you’ll have financial and other resources to rely on at this phase of life.

Possible strategies to pay for care include buying a long-term care plan, setting aside assets that you don’t tap to generate retirement income during your vital years, withdrawing just interest and dividends from savings and preserving principal, and holding home equity in reserve that you can tap when you need it.

However, even if you develop a good strategy to pay for care, you’re not finished. You’ll need someone to help you manage caregivers and manage your money needs. One of my recent projects developed a toolkit for families to use: The Thinking Ahead Roadmap: A Guide to Keeping Your Money Safe As You Age. It’s a publicly available, online resource that was funded and sponsored by AARP, the University of Minnesota and the Society of Actuaries.

Steve Vernon is not affiliated with Northwestern Mutual, and the views expressed by Steve Vernon do not necessarily represent those of Northwestern Mutual or its subsidiaries.

- We proudly protect our loved ones life

- Survived not only five centuries